In my last post in this series, I observed that an economy’s “base” money serves as the “raw material” that commercial banks and other private-market financial intermediaries employ in “producing” deposits of various kinds that can themselves serve as means of exchange.

If they could do so profitably, these private intermediaries would, by making their substitutes more attractive than base money itself, collectively gain possession of every dollar of base money in existence. In some past monetary arrangements, most notably that of Scotland before 1845, banks came very close to achieving this ideal, thanks to the their freedom to supply their customers with circulating paper banknotes as well as with deposits, and to the fact that between them these two substitutes could serve every purpose coins might serve, and do so more conveniently than coins themselves.

All save a handful of commercial banks today are, in contrast, able to supply deposits only, so that only base money itself can serve as currency, that is, circulating money. The extent to which national money stocks have been “privatized,” in the sense of being made up mainly of private IOUs of various kinds rather than officially-supplied base money, has been correspondingly limited, as has the extent to which private money holdings have served as a source of funding for bank loans.

When banks and other private-market intermediaries acquire base money, they do so, not for the sake of holding on to it, as they might were they mere warehouses, but in order to lend or otherwise invest it. More precisely, they do so in order to lend or invest most of the base money that comes their way, while keeping some on hand for the sake of either meeting their customers’ requests for currency, or for settling accounts with other banks, as they must do at the end of each business day, if not more frequently. While banks’ own substitutes for base money may serve in place of base money for all sorts of transactions among non-banks, those substitutes won’t suffice for settling banks’ dues to one another, for every bank is anxious to grab for itself as large a share of the market for money balances as possible, while contributing as little as possible to the shares possessed by rival banks.

Bankers have also learned, through hard experience, that by accumulating the IOUs of other banks, and thereby allowing other banks to accumulate their own IOUs in turn, they expose themselves to grave risks, which risks are best avoided by taking part in regular interbank settlements. Because even the most carefully-managed banks cannot perfectly control or predict the value of their net dues at the end of any particular settlement period, all would tend to equip themselves with a modest cushion of cash reserves even if they did not have to do so for the sake of stocking their ATM’s or accommodating their customers’ over-the-counter requests for cash.

Because banks typically receive fresh inflows of reserves every day, as a result of ordinary deposits, loan repayments, or maturing securities, a responsible banker, once having set-aside a reasonable cushion of reserves, has only to see to it that the lending and investment that his or her bank engages in just suffices to employ those inflows, in order to succeed in keeping it sufficiently liquid. Greater reserve inflows, if judged likely to be persistent, will inspire increased lending or investment, while reduced ones will have the opposite effect.* The bankers’ general goal is to keep funds that come the bank’s way profitably employed, while holding on to just so many reserves as are needed to accommodate fluctuations of net reserve drains around, and therefore often above, their long-run (zero) mean. More precisely, bankers’ strive to keep reserves on hand sufficient to reduce the probability of losses exceeding available reserves to a (usually modest) level, reflecting both the opportunity of holding reserves, which is to say the interest that might be earned on other assets, and the costs involved in making-up for reserve shortages, by borrowing from other banks or otherwise.

Throughout the history of banking, and despite laws that have suppressed commercial banknotes while often imposing minimum (but never maximum) reserve ratios on banks, bank reserves have generally constituted a very modest part of banks’ total assets, and therefore a modest amount compared to their their total liabilities. Indeed, bank reserves have generally been but a small fraction of banks’ readily redeemable or “demandable” liabilities. England’s early”goldsmith” banks are supposed to have held reserves equal to only a third of their demandable liabilities — a remarkably low figure, given the circumstances; at the other extreme, Scottish banks at the height of that nation’s pre-1845 “free banking” episode often managed quite well with gold or silver reserves equal to between one and two percent of their outstanding notes and demand deposits. Modern banks, even prior to the recent crisis, have generally had to keep somewhat higher reserve ratios than their pre-1845 Scottish counterparts, mainly owing to the fact, mentioned above, that they must stock their cash machines and tills with base money, instead of being able to do so using their own circulating banknotes.

Between 1997 and 2005, for instance, U.S. depository institutions’ reserves ranged, with rare exceptions, between 11 and 14 percent of their demand deposits (see figure below). Put another way, for every dollar of base money “raw material” they acquired, U.S. commercial banks were able to “manufacture” (that is, to create and administer) just under 10 dollars of demand deposits. That figure, the inverse of the banking system reserve ratio, is what’s known as the reserve-deposit “multiplier.”

Depository Institutions’ (Demand Deposit) Reserve Ratio, 1997-2005

The multiplier’s significance to monetary policy is, or used to be, straightforward: it indicated the quantity of additional bank deposits that monetary authorities could expect to see banks produce in response to any increment of new bank reserves supplied them by means of either open-market operations or direct central bank loans. If, around 2000 (when the reserve-demand deposit multiplier was about 14), the Fed wanted to see bank’s demand deposits increase by, say, $10 billion, it had only to see to it that they acquired $(10/14) billion in fresh reserves, which meant creating a somewhat larger quantity of new base dollars — the difference serving to make up for the tendency of some of any newly created bank reserves to be converted into currency. The ratio of the total amount of new money, including both currency and bank deposits, generated in response to any new increment of base money, to that increment of base money itself, is known as the “base money multiplier.”

Since the recent crisis, all sorts of nonsense has been written about the “death” of the reserve-deposit and base-money multipliers, and even (in some cases) about how we ought to be glad to say “good riddance” to them. I say “nonsense” because, first of all, the multipliers in question, being mere quotients arrived at using values that are themselves certainly very much alive, cannot themselves have “died,” and because the working of these multipliers does not, as some authorities suppose, depend on the particular operating procedures central banks employ. Finally, although it’s true that, until the recent crisis, economists were inclined, with good reason, to take the stability of the reserve-deposit and base-money multipliers for granted, it doesn’t follow that they (or good ones, at least) ever regarded these values as constants, as opposed to variables the values of which depended on various determinants that are themselves capable of changing.

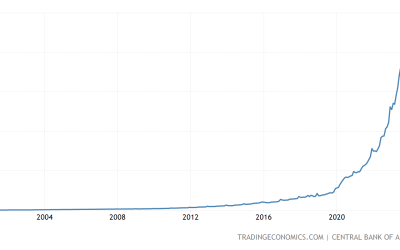

What certainly has happened since the crisis is, not that the reserve-deposit and base-money multipliers have died, but that their determinants have changed enough to cause them to plummet. U.S. bank reserves, for example, have (as seen in the next picture) gone from being equal to a bit more than a tenth of demand deposits to being about twice the value of such deposits! The base-money (M2) multiplier, shown further below, has, at the same time, fallen to below half its pre-crisis level, from about 8 to 3.5 or so (not long ago it was less than 3).

The Reserves-to-Demand-Deposits Ratio Since 2005

The Base-Money M2 Multiplier since 2005

These are remarkable changes, to be sure. But they are hardly inexplicable. Banks’ willingness to accumulate reserves depends, as I’ve already noted, on the cost of holding reserves, which itself depends on the interest yield of reserves compared to that of other assets banks might hold instead. Before the crisis, bank reserves earned no interest at all. On the other hand, banks had all sorts of ways in which to employ funds profitably, especially by lending to businesses both big and small. Consequently, banks held only modest reserves, and bank reserve and base-money multipliers were correspondingly large.

The crisis brought with it several changes that are more than capable of accounting for the multipliers’ collapse. The recession itself has, first of all, resulted in a general reduction in both nominal and real interest rates on loans and securities, to the point where some Treasury securities are now earning negative inflation-adjusted returns. Regulators have in turn responded to the crisis by cracking-down on all sorts of bank lending, making it costly, if not impossible, for banks, and smaller banks especially, to make many of the higher-return loans, including small business loans, they would have been able to make, and to make profitably, before the crisis. (More here.) U.S. bank regulators have also begun to enforce Basel III’s new “Liquidity Coverage Ratio” rules, compelling banks to increase the ratio of liquid assets, meaning reserves and Treasury securities, to less-liquid ones on their balance sheets. Finally, since October 2008, the Fed has been paying interest on bank reserves, at rates generally exceeding the yield on Treasury securities, thereby giving them reason to favor cash reserves over government securities for all their liquidity needs.

Whatever their cause, today’s very low money multiplier values mean that commercial banks have ceased to contribute as they once did to the productive employment of scarce savings. Instead, those savings have been shunted to the Fed, and to other central banks, which use them to purchase government securities, and also for other purposes, but never, with rare exceptions (and with good reason), to fund potentially productive enterprises. Although discussions of monetary policy since the crisis have mainly had to do with the quantity of money, and central banks’ efforts to expand that quantity so as to stimulate spending, the effects of the crisis, and of governments’ response to it, on the quality of money, and especially on the investments its holders have been funding, deserve at least as much attention.

______________________

*Besides funding loans with retail deposits banks can and do fund them by borrowing on wholesale markets. In that case, loans may be arranged in anticipation of a bank’s acquisition of funds. Either way, banks must acquire base-money sufficient to finance their lending (that is, to cover their settlement dues) if they are to avoid having to rely too often on funding from last-minute interbank loans.

This post first appeared first on Alt-M.